KUALA LUMPUR: Duopharma Biotech Bhd is expected to see steady revenue growth predicted by the recovery of consumer healthcare (CHC) sales and the recent renewal of the approved product purchase list (APPL) tender, said RHB Research.

The research house said Duopharma has seen an encouraging pick-up in the local sales segment, indicating sluggish consumer demand for CHC products has bottomed.

"Moving forward, the group expects CHC segment growth to be largely driven by analgesic products (i.e., painkillers) as well as its regional expansion to drive vitamin C sales (i.e., Flavettes, Champs, and Proviton)," it said in a note.

Meanwhile, RHB Research said Duopharma also intends to expand its CHC product offerings to reduce its reliance on vitamin C sales.

The group has set up its regional office in Indonesia (with the wholly-owned subsidiary incorporated in April 2023), spreading its regional footprint to a third country after Singapore and the Philippines.

"Duopharma's immediate objective is to provide contractually manufactured oral solid dosage products (OSD) to the Indonesian market," it said.

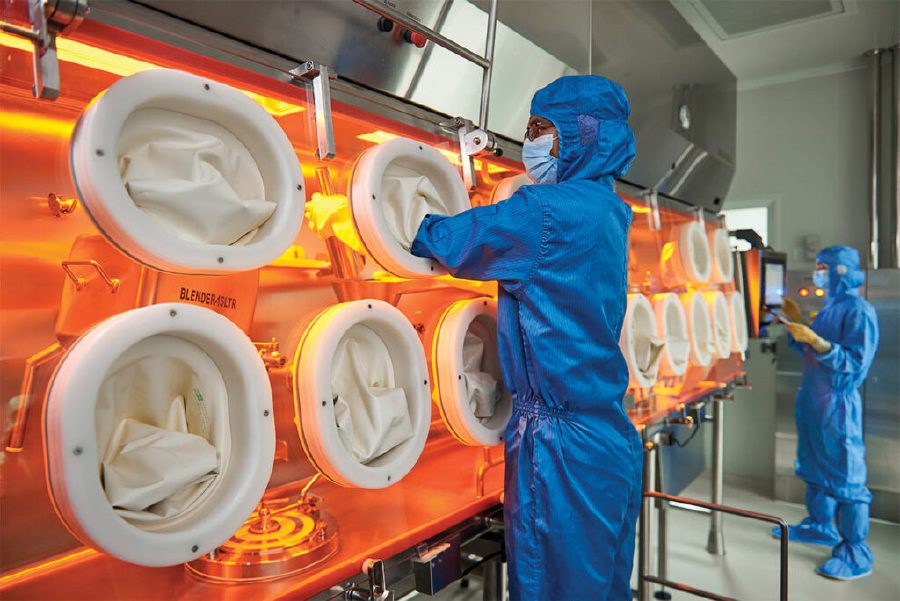

On the company's capital expenditure (capex), RHB Research said that following the receipt of the certificate of completion (CCC) of its K3 facility in July 2023, Duopharma guided that its 2024 capex spending is expected to be lower than 2023 as most expansions near the tail-end.

The firm said the remaining capex is expected to be channeled towards expanding biologics manufacturing capabilities at K5, using the available space (40,000 sq ft) in the K2 facility for injectable drugs, and upgrading its Highly Potent Active Pharmaceutical Ingredient (HAPI) facility to secure EU GMP certification by the end of 2024.

All in all, RHB Research has trimmed its financial year 2024 (FY24) to FY25 earnings forecast by 12 per cent and 13 per cent as the CHC sales recovery was below its expectations, offset by an uptick in public sector sales.

"We also lowered our capex assumption to align with management's guidance.

"Post adjustment, maintain buy on the stock with our target price now higher at RM1.44 from RM1.41," it added.