SYNDICATES led by unscrupulous repossessors are exploiting bank records to repossess vehicles with outstanding loans. The minutes they have possession of the vehicles, they orchestrate the illegal sale.

The modus operandi of the syndicates is to put on a helpful front, assuring loan defaulters that their vehicles would be well cared for. And that this was an alternative to being blacklisted by banks.

Some would also offer to help find new buyers, promising loan defaulters the minimum amount of compensation.

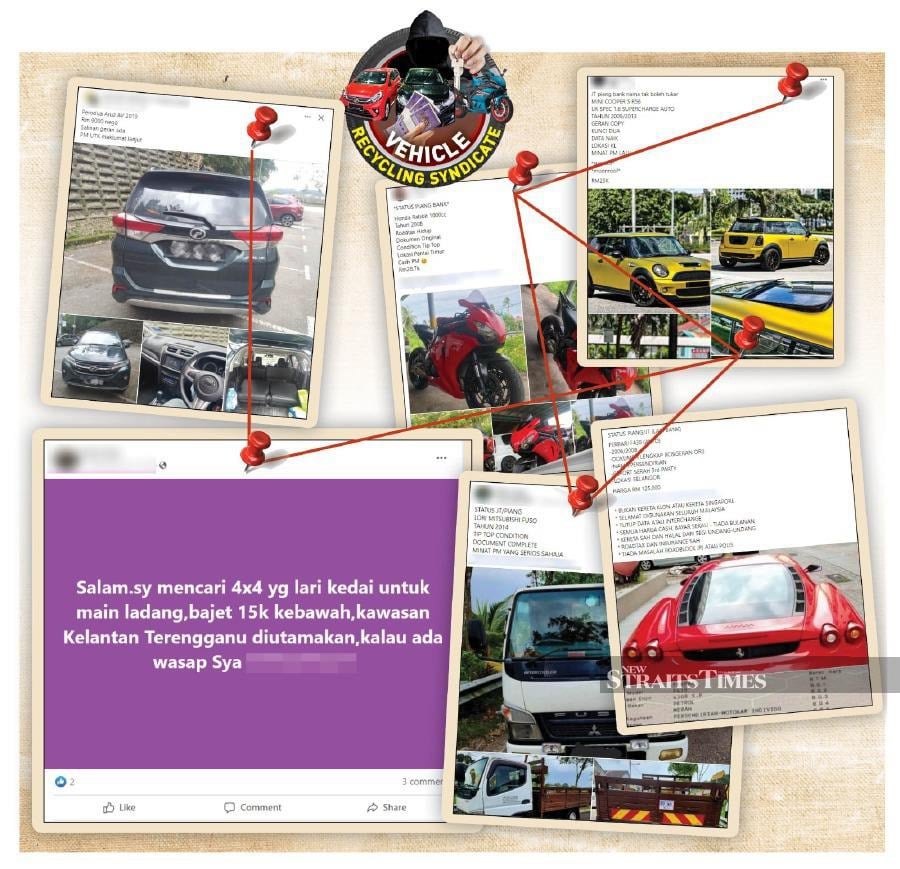

The NST Focus' months-long investigation found that these "recycled" vehicles, are commonly referred to as kereta jalan terus (JT) or kereta logo. They would be resold at between 50 and 75 per cent below their market worth.

Sometimes, these vehicles are also known as kereta piang.

To be specific, kereta JT means repossessed vehicles sold in cash, kereta piang refers to cars sometimes sold in a "loan takeover" concept known as sambung bayar, and kereta logo stands for those with "protection" stickers under the watch of gangsters.

Checks revealed the presence of multiple groups on social media platforms, with some requiring private invitations from the account holders to join in.

Some of the groups were promoting repossessed vehicles, which included motorcycles and lorries, to buyers in Indonesia and Singapore.

Besides individuals who could not qualify or have been blacklisted from getting loans, these vehicles are also coveted by criminals and workshop owners, who would use them to commit crimes and cannibalise them for spare parts, respectively.

Our investigation also revealed the involvement of secret societies that provided "protection stickers" for these vehicles.

The stickers, costing between RM100 and RM2,000 per month depending on model, serve as a warning to legal repossessors to dissuade them from legally recovering these vehicles for banks.

Legal industry insiders alleged that some syndicates might even have the police on their payroll.

Legal vehicle repossessors whom NST Focus spoke to revealed that they had to cross state lines to file reports — an obligatory procedure whenever a vehicle is being repossessed — because some local police stations refused to accept their reports.

Besides stickers, syndicate members also offered buyers of these outstanding loan vehicles their services to legally transfer the vehicle registration for prolonged usage, or pay an extra fee to have their registration numbers "removed" from the repossessor's database.

However, checks revealed that there was no formal database for vehicle repossession, and most repossessors were relying on their own makeshift systems compiled from repossession orders issued by various banks.

This meant that a bank's repossession orders for specific vehicles could never be revoked, only temporarily "hidden" or "ignored" by the agents.

"This outstanding multi-purpose vehicle (a Toyota Alphard) is in Kuala Lumpur.

"If you want to use it outside of the city, it is best to close the data (hide the repossession instruction) or use a protection sticker. But it is hard to transfer the vehicle registration because we are unable to trace the owner. So it is better to close (hide) the repossession data (of the vehicle from the repossessors' database).

"The vehicle price is RM27,000. To hide the registration number from our (repossession) system costs RM2,000, so the total sale price is RM29,000," said a broker whom the reporters spoke to.

Other offers included a 2017 Honda BRV for RM23,000 (market value RM60,000), a Honda Jazz with two-digit registration numbers for RM20,500, a 2018 Vellfire Robot 2.5 for RM58,000 (market value RM200,000), and a 2018 Perodua Axia for RM7,000 (market value RM25,000).

Additionally, there is a 2020 Yamaha Y15 150cc motorcycle available for RM3,300 (market value RM7,000), a 2023 Honda Vario 160cc priced at RM4,800 (market value RM10,000), and a 2022 Yamaha LC135 135cc motorcycle for RM4,300 (market value RM7,000).

Only cash payments were accepted, given that the loans of these vehicles were in default.

When asked why some defaulters were willing to sell their vehicles and potentially face blacklisting by banks, the broker said many did so for the money.

"Instead of allowing the bank to auction off their vehicles, which they still have to service the remaining loan sum and continue to be in debt, they might as well sell them to us.

"At least they will get a few thousand ringgit," he said.

Under the Insolvency Act 1967 amended in 2020, loan defaulters could only be declared bankrupt if their outstanding debt reached RM100,000.

The NST learnt that in their attempt to avoid being blacklisted, many of these deadbeats would lodge reports, claiming that their vehicles had been stolen.

"The defaulters will give a time frame, maybe a month for the broker to 'settle' their cars before lodging a report.

"So normally, these defaulters will declare beforehand to the broker their intent to lodge a stolen vehicle report and claim insurance.

"That means the car would be blacklisted by the police and may only be used for spare parts," a source said.

Another broker whom NST reporters met referred to this type of vehicle as kereta claim.

"We no longer accept kereta claim because there is no point in buying it if we can't use it on the road," he said.