KUALA LUMPUR: Malaysia is expected to bounce back from its low foreign bond and equity position with a bottoming out of interest rate differentials with the US.

An easing of monetary policy by major central banks are a key catalyst for increased foreign capital inflows.

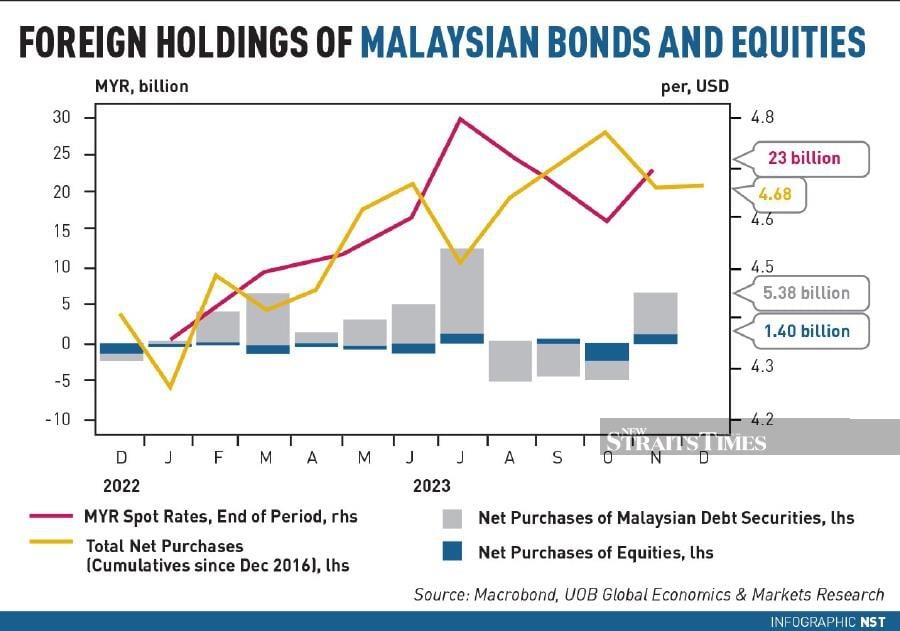

According to Standard Chartered Bank Singapore's report on ASEAN currencies by ASEAN and South Asia chief economist Edward Lee and Economist Asia, Jonathan Koh, foreign allocation to Malaysia bonds is 2.2 percentage points below index-neutral levels and 0.5 percentage points lower than historical mean allocation levels, while foreign equity outflows for Malaysia stood at US$6 billion in 2023.

Foreign ownership of Malaysia's local bond markets stood at 35 per cent.

"The anticipation for monetary easing by the major central banks are the key catalyst. The carry trade is likely to be reversed i.e. borrowing on low interest rate currency and investing in high interest rate currency would be shifting," Bank Muamalat Malaysia Bhd chief economist Dr Mohd Afzanizam Abdul Rashid told Business Times

"So emerging currencies including ringgit should be benefiting from this trend," he added.

Afzanizam said there is a positive relationship between ringgit and foreign ownership in equities.

"This would mean the expectation for a strong ringgit would entice foreign investors to come and invest in Malaysian equities," he said.

Standard Chartered expects the ringgit to be an outperformer in 2024, after having the distinction of being the only ASEAN currency to end 2023 weaker than the US dollar on a nominal effective exchange rate (NEER) basis.

It expects the ringgit to hit 4.40 against the greenback by end of 2024.

Two factors however limit its upside. "First, based on our projections, US policy rates could remain historically high versus ASEAN economies by end-2024. Second, ASEAN central banks may also cut rates, particularly those who had hiked partly to stave off foreign exchange weakness," Standard Chartered said.

It expects the interest rate differentials between the US and Malaysia to improve.

"The year ahead with stable global economic prospects, a decent domestic economic outlook and an equity market yet to recover and along with a relatively weaker ringgit can drive inflows not only aiding ringgit gains but also equity market gains and keeping bond market yields largely stable," Independent economist Julian Suresh Sundaram told the Business Times.

"We are observing the returns of foreign investment back to the Malaysia bourse, although it was not significant but it was consistent.

"This is due to the fact that the fund managers were closely monitoring the action of the Fed chairman that continuously insisted on the possibility of further increase in order to achieve the targeted 2 per cent inflation rate, which at the moment hovers at 3 per cent," said Universiti Kuala Lumpur Business School economic analyst Associate Professor Aimi Zulhazmi Abdul Rashid.

Aimi believes the Malaysian stock market is undervalued, especially when considering its historical performance. "Malaysian bourse can be considered as undervalued.

In January 2022, the index exceeded 1500 points but since then the index has been hovering around the1400 to 1450 points for almost 2 years.

"Malaysia's large corporations are doing good business and recording healthy profits from banking and finance, oil and gas, telecommunication and even construction companies rebounded in 2023.

"This would attract foreign fund managers to the Malaysian bourse," he said.