KUALA LUMPUR: Genting Malaysia Bhd's continued recovery of its key Malaysian operations, contributing about 62 per cent of total revenue for the first half (1H) of 2023, will drive robust earnings growth for the coming quarters.

CGS-CIMB Research, in a note, said Genting Malaysia's 3-year earnings-per-share (EPS) will see a compounded annual growth rate (CAGR) of 42 per cent in FY22–25, based on the research firm's estimates.

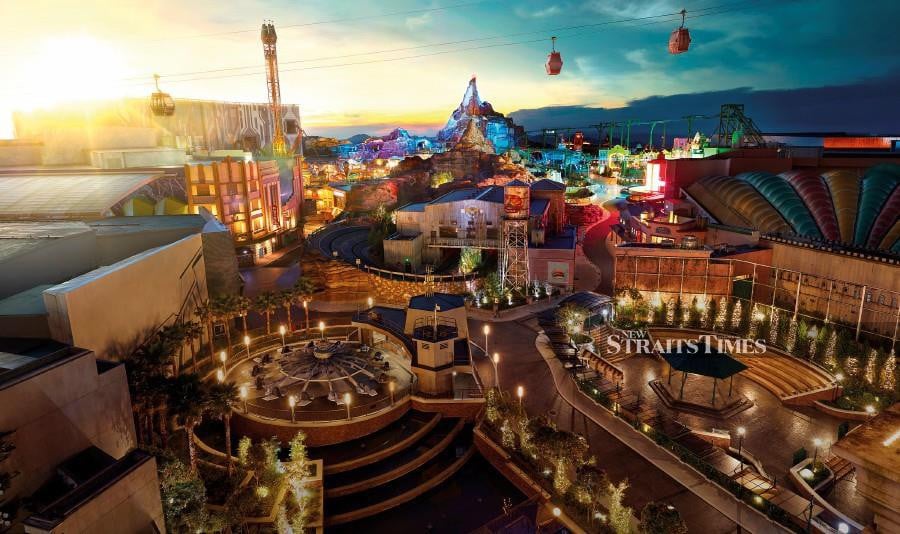

"Findings from our visit suggest that both domestic and foreign tourist arrivals are on the path to full recovery while operating capacity has primarily returned to pre-pandemic levels.

"We observed that non-gaming activities, such as restaurant dining and the indoor theme park, were largely packed, and SkyWorlds, the outdoor theme park, was busy with ongoing promotional campaigns.

"Based on our observation, Resorts World Genting's (RWG) casino capacity seems to be fully restored to pre-pandemic levels, with more slot machines and gaming tables that are well-manned across both gaming floors, evidence of the easing of the croupier shortage," CGS-CIMB Research said.

This puts RWG in good stead to benefit from the seasonally higher fourth quarter (Q4) of 2023 and the first quarter (Q1) of 2024 traffic as tourist arrivals continue to pick up, the research firm noted.

Further, CGS-CIMB Research also estimates that the improving revenue generation on higher visitations should allow RWG's EBITDA margin to come in above Genting Malaysia's guidance of 30-33 per cent for FY23, with Q2 2023/1H23 EBITDA margins at 34.7 per cent/33.0 per cent.

Touching on the company's United States (US) casino operations, CGS-CIMB Research views the revival of the New York State Gaming Commission's (NYSGC) request for application (RFA) process on August 30, 2023, after a 6-month halt for three downstate New York commercial casino licenses as a major re-rating catalyst for Genting Malaysia.

The research firm believes Resorts World New York City (RWNYC) is a frontrunner.

This is given RWNYC's ability to generate extra gaming taxes for the state almost immediately, as existing floor space is ready to deploy 200–250 live table games versus a new casino and its long-term operational track record in the area.

"We believe that should RWNYC win a license in 2024, the minimum required capital of US$1 billion could be funded by the potential sales proceeds of its Miami land, for which it has received an offer of over US$1.23 billion.

"As such, we estimate this could lift our fair value by 8–14 per cent to RM4.32-RM4.55," it said.

CGS-CIMB Research retains its 'Add' call on Genting Malaysia, with a preferred pick for the revival of Malaysia's tourism sector, with an unchanged target price of RM4.00.

"At our target price, Genting Malaysia would be trading on 21x 2024 price-to-earnings (P/E) ratio and offers a 4 per cent dividend yield.

"Downside risks include higher-than-expected operating costs and slower Malaysian gaming revenue recovery," CGS-CIMB Research said.